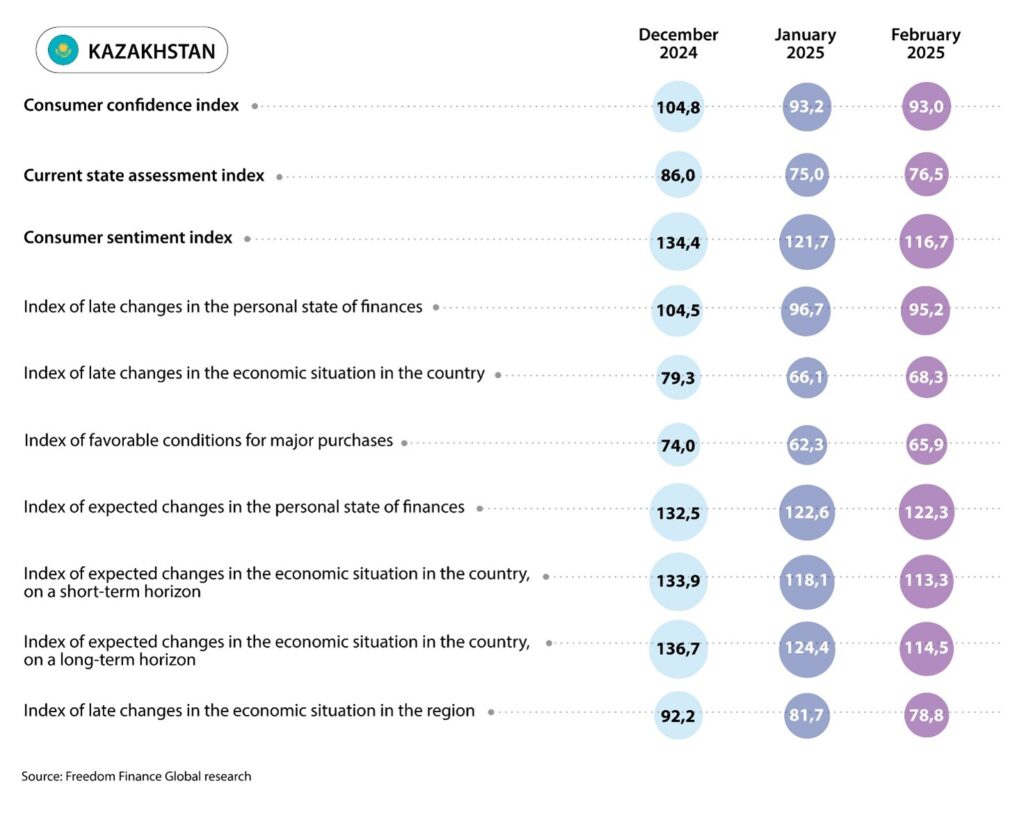

Freedom Finance Global has been researching consumer confidence, inflation and devaluation expectations of Kazakhstan residents for the past twenty-eighth month. In February 2025, the Consumer Confidence Index (CCI) remained neutral at 93 points, marking the second consecutive time it reached the lowest value in the history of the research. Negative responses continue to outweigh positive ones. Optimism regarding economic forecasts has noticeably declined again. However, a slight recovery is observed in a couple of other components. Inflation estimates have been rising for the fourth month in a row amid accelerating official inflation and worsening export forecasts. Inflation expectations remained at the same level, as did devaluation expectations, amid a noticeable strengthening of the tenge.

Analysts collect 3,600 questionnaires monthly in Kazakhstan, providing a sufficient sample to assess various parameters. The research is based on a methodology used to obtain consumer confidence indexes in many countries around the world and adapted to local needs by the United Research Technologies Group. Data collection method: telephone survey. The survey questionnaire is localized: the research is conducted in the native language of the respondents.

Residents’ economic forecasts worsen again

The sub-index for the economic outlook over the next 12 months decreased by 5 points, reaching its lowest level since June 2023. This marks the second consecutive month of a sharp decline in this indicator. The share of those who believe that the economic situation will improve fell from 45% in January to 40% in February.

Across all age groups, a monthly decline in optimism was observed everywhere except for people over 60. The most noticeable deterioration is recorded among respondents aged 45-59, where the share of optimistic respondents fell from 43.5 to 33.1%. This indicator is the worst among all age groups. The share of those expecting an improvement in their economic situation also fell among respondents aged 30-44 by slightly less than 6 p.p. Young people under 29 remain the most optimistic age group, with 45.1% expecting improvement. This was also a noticeable decline compared to January. However, among the older generation over 60, a slight increase in optimism was recorded: the same share indicator increased from 39.5 to 41.6%.

At the regional level, a decrease in optimism regarding forecasts of changes in the economic situation is observed in 15 out of 20 regions. The biggest surprise came from the Ulytau region, where the share of positive responses increased from 43.8% to 60.7%. This result turned out to be the best in February among the regions. The share of people expecting economic improvement over the next year also increased quite well in the West Kazakhstan region (+8.4 p.p.) and Almaty Region (+7.2 p.p.). The largest decrease in the share indicator and the worst result in February were recorded in the North Kazakhstan region: the indicator fell from 45.7 to 25.9%. A significant decrease of more than 10 p.p. per month is also observed in the regions of Astana, Kostanay, Pavlodar and East Kazakhstan.

Conditions for large purchases have slightly recovered

The sub-index measuring favorable conditions for large purchases increased by 3.7 points compared to January and reached 65.9 points. This recovery followed the lowest value in the history of the survey recorded in January. The share of Kazakhstanis who believe that the current conditions for large purchases are favorable fell from 26.4 to 25.9%. However, this time, the growth of the sub-index was ensured by a noticeable drop in the share of pessimists: from 66.4% to 63.3%.

Among the age groups, respondents aged 45-59 showed the greatest drop in pessimism. Among them, the share of negative answers fell from 70.3% to 64%. Young people under 29 also showed a noticeable improvement, among them, the same indicator fell from 60.9 to 57.5%. This became the best indicator of February among all age groups. On the other hand, we note a small monthly increase in the share of those noting the unfavorability of current conditions for large purchases among the older generation over 60: from 67.1 to 68.3%.

In the regional context, improvements are observed in all regions except the Akmola, Mangystau, Kostanay and Kyzylorda regions. In these regions, the share of negative responses increased compared to January. The most noticeable growth occurred in the Mangystau (+8.6 p.p.) and Kostanay (+6.7 p.p.) regions. However, residents of the Kyzylorda region gave the worst responses again, where the share of those who consider current conditions generally unfavorable for large purchases reached 72%. On the other hand, the share of negative responses fell by more than 10 p.p. in three regions at once. The largest decrease was recorded in the Ulytau region: 23 p.p. As a result, the best result of this month was shown by the Ulytau region, where the share of negative responses was only 45.3%. Also, the same indicator fell by almost 13 p.p. in the Pavlodar and Aktobe regions.

Slight recovery in economic assessments

The sub-index of changes in the economic situation over the past 12 months also recovered slightly by 2.2 points after the record low for the entire research in January. The share of those who believe that the economic situation has improved over the past year increased from 13.3% in January to 14% in February.

Among the age groups, the monthly increase in optimism is observed only in two groups. However, their growth rates were quite noticeable. The share of those who noticed an improvement in the economic situation in the country increased from 13.9% to 17.1% in a month among young people under 29. This was the best value for February among all age groups. The share of positive responses among the older generation over 60 also increased by 3 p.p. On the other hand, the same indicator fell from 12% to 9.9% among respondents aged 45-59, which is the worst result of this month.

In the regional context, monthly improvement of indicators is observed in 12 out of 20 regions. Once again, the residents of the Ulytau region, who also showed the best dynamics, gave the best answers. Among them, the share of those optimistic about changes in the economic situation increased from 14.2% to 26%. The same indicators also increased by 5-6 p.p. in the Zhambyl, West Kazakhstan regions and the city of Shymkent. On the other hand, the most noticeable deterioration in the share of positive answers is recorded in the Mangystau region: from 20.3% to 12.8%. The similar share also noticeably fell in the Akmola region, where it reached only 7.3%. However, the Atyrau region gave the worst answers again, where this figure was only 6.6%, which is 0.5 p.p. less than in January.

Residents’ inflation estimates continue rising

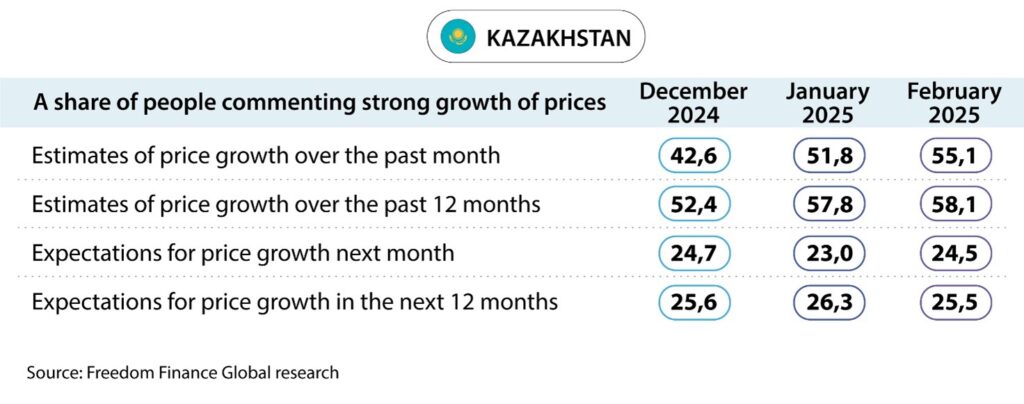

Inflation estimates of Kazakhstan residents have been showing growth for the fourth month in a row, although this time, the increase was not so significant. Over the past month, 55.1% of respondents (51.8% in January) indicated a strong increase in prices. As a result, this indicator reached its maximum since April 2023. And the share of people who noticed a rapid increase in prices over the previous 12 months has not grown so significantly: from 57.8% in January to 58.1% at the time of the last data collection.

But the inflation expectations of Kazakhstanis as a whole showed a neutral result, in contrast to inflation estimates. The share of people expecting a strong increase in prices in the one-month horizon increased from 23% to 24.5%, while in the next 12 months horizon, the share of those expecting an acceleration in price growth fell slightly from 26.3% in January to 25.5% at the time of the last survey.

Similar research of inflation estimates and expectations performed by the National Bank of Kazakhstan demonstrated a much greater increase in pessimism in February. According to the data presented, the share of those expecting a strong price increase during the year increased from 26.9% to 29%. In the one-month horizon, the same indicator sharply increased from 23.3% to 29.2%. In general, a reverse increase in pessimism is recorded after its sharp fall in January. Inflation estimates continue to grow for the fourth month in a row, as is the case with our research. If the share of respondents noticing a strong price increase over the past month increased from 39.4 to 46.1%, then the share of those indicating a rapid price increase over the previous 12 months increased from 47 to 53.1%.

Among certain goods and services, the majority of Kazakhstanis continue to be concerned about the significant increase in food prices. However, this time, for the first time during the research, housing services and utilities were among the top 3 goods and services most noticeably increased in price, according to the residents. Almost 35.7% of respondents noticed a strong increase in tariffs for housing services and utilities (24.9% in January). We also note the return of ‘Meat and Poultry’ to first place after a month-long break. This product was chosen by 54.3% of the surveyed residents against 43.5% in January. In addition, the residents continue to be concerned about vegetables and fruits. For them, the share of people who noticed a strong increase in prices was 50.8%, which is only 2 p.p. lower than the record value of January. We observe a significant rise in concern over a number of goods and services. Particularly noticeable growth occurred for ‘Internet and Mobile Communications’ and ‘Medicines and Drugs’. According to official statistics, prices for vegetables and fruits rose by an average of 3.5% month-on-month (MoM) in February after almost the same growth in January. Prices for meat and poultry also rose very significantly: by 2.4% per month. The last time such a strong monthly increase in prices for this product was observed in March 2022, when, in principle, prices for almost all items rose sharply. Housing services and utilities tariffs increased by another 3% MoM in February and over the year showed a 16.3% growth, which significantly outpaces overall inflation.

Devaluation expectations remained at the same level

Devaluation expectations of Kazakhstanis generally remain at the same level as in January. The dollar exchange rate fell by almost 4% in February, which certainly stopped the growth of pessimism among the residents. According to the research, the share of Kazakhstanis expecting the tenge to weaken over the one-year horizon fell from 61.3 to 59.4%; and over the month horizon, it increased slightly from 39.1 to 40.4%.

Conclusions

The second month of 2025 continues to be negative in terms of consumer confidence among Kazakhstanis. After a sharp drop in January, the index continues to be below 100 points, indicating that negative responses outnumber positive ones. Once again, there is a renewed decline in the public’s forecasts regarding the economic situation, which has reached the lowest level in the past 20 months of observation. During this period, few Kazakhstanis have expressed optimism about economic improvement in the coming year. However, there is a slight recovery in terms of the favorableness of current conditions for large purchases and assessments of changes in the economy. Yet, these indicators continue to be near record lows. In absolute terms, Kazakhstanis are still very concerned about the economic situation, given the recent discussion of the increase in value-added tax, the rise in the dollar exchange rate and the overall increase in inflationary pressure, which more and more residents have begun to notice.

In February, the dynamics of inflation estimates and expectations were again negative, given the continued growth of inflation estimates for the fourth month in a row. Amid the acceleration of official annual inflation to 9.4%, which is the highest value since February 2024, it is not surprising to see a continued growth of inflation estimates. In addition, the dynamics of this indicator are similar to a comparable survey by the National Bank in recent months. Housing services and utilities are one of the main drivers of price growth, which did not go unnoticed by the residents. Moreover, the recent seasonal increase in prices for vegetables and fruits continues to affect sentiment. Yet, inflation expectations remained at approximately the same levels. That is, Kazakhstanis continue to consider the current price increase as temporary. This is probably also facilitated by the sharp decline in the dollar exchange rate in February. Devaluation expectations, however, did not decrease so significantly and generally remained at the January level. We probably need a slightly longer period of stability in the dollar exchange rate, after which we will see a reduction in these expectations.

As a result, the 28th wave of the Kazakhstanis consumer confidence research showed a neutral result after a sharp drop in January. However, this did not save from updating the minimums for one of the index components. As in January, Kazakhstanis remain very worried about the economic situation in the country. The deterioration of inflation forecasts from experts and the National Bank for this year, together with the actual acceleration of inflation, may exert further negative pressure on the consumer confidence of Kazakhstanis. Nevertheless, there is some hope for a strengthened tenge, which, with some delay, may positively affect inflation expectations and generally help consumer confidence show signs of recovery.